That’s the hole many retirees say they’ll feel by 2026, even after chunky increases from the triple lock. It’s not a headline scare. It’s the slow scrape of lost pounds over real winters, real bills, real choices.

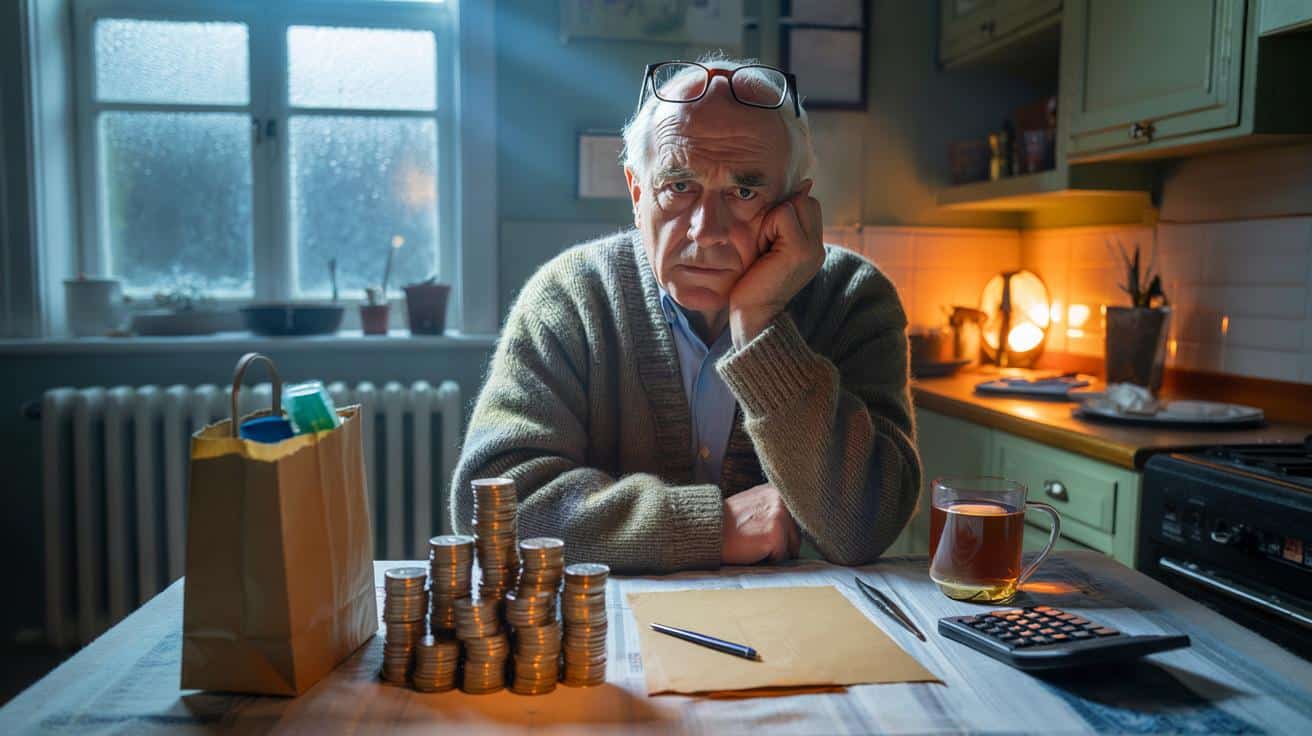

It’s a Thursday morning in a damp church hall in Derby, and the radiator under the window clicks on as the coffee queue shuffles forward. George, 72, is tracing numbers on an old envelope, adding next April’s State Pension, then taking away council tax, the energy direct debit, his phone. He does it every month, with the same biro, like a ritual he never asked for. Across the room, someone jokes about “the Chancellor’s invisible hand” adjusting their thermostat. No one laughs for long.

George says the rises feel big on paper, yet smaller in the fridge. He’s not angry. Just tired of the maths. The gap nags.

The £2,933 gap, explained without the jargon

Let’s put a shape around that gap. Think of it as a running tally of missed uplift, frozen tax thresholds, and bills that keep quietly re-basing higher. In 2022-23, the triple lock was suspended for one year, so State Pension rose by 3.1% rather than earnings of roughly 8%+. A small decision at the time, said to be temporary. It left a permanent notch in the income ladder for anyone on the full pension.

That notch compounds. Every later rise starts from a lower base, and frozen tax bands bite harder as pay and pensions creep up. The result isn’t dramatic on any single morning. It shows up in a winter of thicker socks and supermarket swaps. **The £2,933 gap** is a way to count that feeling with a number that’s big enough to matter, small enough to miss in headlines.

We’re not talking about a theoretical pain. We’re talking about a real-world shortfall by 2026 for many people on a full new State Pension, compared with where they’d likely stand if the triple lock hadn’t been paused, and if tax thresholds moved with prices. Not doom. Just sums.

Take Eileen, 69, full record, new State Pension. In 2021-22 her weekly pension sat just under £180. The following April delivered 3.1% instead of what would have been about 8%+, leaving her roughly £450 short that year. The next rises landed on that smaller base, so the gap didn’t vanish. It quietly grew. Then came higher energy, groceries up double digits at points, and insurance premiums that refuse to sit still.

Now add the tax trap. The personal allowance is stuck at £12,570 through at least 2027-28. State Pension rose strongly in 2023 and 2024, and might climb again. By 2026, many with modest extras — a small works pension, a sliver of savings interest — drift into income tax on money that used to be tax-free. That’s another nibble, not a chunk, yet nibbles add up.

Stack those pieces and you land near a three-figure hit in 2022-23 that compounds through each year and is joined by threshold creep. On a cautious estimate, the running loss by April 2026 for someone like Eileen sits around **£2,933** compared with a world where the triple lock never blinked and tax bands kept pace. It’s not every pensioner, and not exact to the pound. It’s a fair yardstick for the pressure you can feel but can’t always see.

How to shrink that hole before it swallows your winter

Start with what’s in your gift. Check your National Insurance record for gaps since 2006 and consider topping up missing years with Class 3 contributions if it boosts your State Pension. It’s not glamorous, yet the return can be striking for certain years. Then look at Pension Credit even if you think you’re just above the line. It opens a door to council tax support, NHS dental and glasses help, and the Warm Home Discount in many cases.

Next, trim what’s quietly sprung. Ask your council about a Single Person Discount if you live alone. Query your energy supplier for a better direct debit and an accurate meter read. Review home insurance at renewal; loyalty pricing is back in disguise. If you have a private pension pot, a small reshuffle of withdrawals across tax years can cut the tax you pay. *Tiny moves, real pounds.*

We’ve all had that moment where the admin pile stares back, and you close the drawer. **Let’s be honest: nobody tracks CPI in a notebook.** So pick one action this week, one next week. People miss out not because they don’t care, but because forms feel hostile, phones ring forever, and it’s easy to believe “this won’t apply to me.” It might. It often does.

“The single biggest mistake we see is pride getting in the way of Pension Credit,” says Ruth, a caseworker at a local advice centre. “It’s not charity. It’s part of your pension. Once people claim, doors open.”

- Check Pension Credit eligibility in 10 minutes on gov.uk. A successful claim can passport you to extra help.

- Ask your council about Council Tax Reduction and one-off hardship funds.

- Apply for the Warm Home Discount if your supplier participates.

- Review savings and ISAs: shift taxable interest into ISA space where possible.

- Consider deferring your State Pension if you’re still working and don’t need it yet. A pause can lift your weekly rate later.

What 2026 could look like, and why it matters now

By April 2026, the new State Pension may sit much closer to the frozen personal allowance. A lot depends on inflation readings and wage growth this autumn and next. The triple lock could deliver another sizeable bump, or a calmer one. Either way, frozen bands mean more pensioners pay tax on slices of income that once slipped below the radar.

That tax drag meets stubborn bills. Energy isn’t racing like 2022, yet prices haven’t fallen back to the old normal. Council tax caps are higher than they used to be, social care levies are baked in, and food inflation tends to settle at a higher base. Some households will feel okay. Some won’t. The gap isn’t only arithmetic. It’s also confidence.

The honest twist: there’s time to tilt this your way. Claim what’s yours. Move what you can. Nudge providers. Vote with questions at hustings and surgeries. The £2,933 figure isn’t destiny. It’s a prompt to plan with eyes open and a list on the fridge.

| Point clé | Détail | Intérêt pour le lecteur |

|---|---|---|

| What drives the £2,933 gap | 2022 triple lock pause, compounding effect, frozen tax thresholds, higher base costs | Understand where the shortfall comes from and whether it applies to you |

| Who is most exposed | Full State Pension recipients with small private income, modest savings interest, and no Pension Credit | See if your household sits in the risk zone by 2026 |

| Practical fixes now | Pension Credit checks, NI top-ups, council tax help, energy discounts, tax-efficient withdrawals | Actionable steps to recover hundreds without cutting essentials |

FAQ :

- How did you calculate the £2,933?By comparing a typical full new State Pension path with the one-year pause in 2022-23 against a counterfactual where the earnings element had applied, then rolling that difference forward and adding likely tax from frozen thresholds by 2026 for someone with small extra income. It’s an estimate, not a promise, but it fits what many households report.

- Will I pay tax on my State Pension by 2026?If it’s your only income, you may still be under the £12,570 allowance. Add a small works pension, part-time earnings or taxable interest, and you could cross the line. The allowance is frozen, so more people drift into tax each year.

- Is the triple lock safe?Both big parties say they support it. Future upratings still depend on CPI and earnings readings each September and on policy choices after the election cycle. Plan for volatility, not certainty.

- Should I defer my State Pension?Deferral can raise your weekly rate later, which helps if you’re working and don’t need the income now. It’s a personal calculation: health, tax position, other income, and your break-even age all matter. Get guidance before deciding.

- What does Pension Credit actually do?It tops up low incomes and often unlocks other support: council tax help, Warm Home Discount, NHS costs, sometimes free TV licences at 75. Even a small award can trigger big savings. Check eligibility in minutes.

Helpful piece. Quick question: does the £2,933 estimate assume CPI and earnings follow OBR central forecasts? If inflation undershoots or energy tariffs fall faster, how much would that shrink the gap? A sensitivity band (best/central/worst) would make this even stronger.

So the Chancellor’s “invisible hand” is adjusting my thermostat and rummaging in my biscuit tin now? 🙂 Asking for a friend called George.